The 4 Most Common Mechanisms for Double Tax Relief on Short-Term Assignments

Many global companies are using short-term assignments to meet talent requirements for projects and skill gaps for short periods of time. (…)

(…) As a matter of fact, 55%* of companies said they expected the number of short-term assignments to increase over the coming year. Short-term assignments may be appealing as a company does not have to pay to relocate an entire family and the tax bill can be lower. The key word here is „can“, as there are a number of complexities involved in taxation of short-term assignments.

Taxing Short-Term Assignments

Due to the brief nature of short-term assignments, the employee typically maintains their home country tax residency, which has an impact on the taxes owed. The employee/company may be exposed to potential double taxation where the same earned income is taxed in both the home and host locations. As a result, most countries offer double tax relief.

What is Double Tax Relief?

Double tax relief is exactly what it sounds like — a means to minimize your tax exposure to avoid paying full taxes in both the home and host locations. There are four ways to claim double tax relief and calculating them by hand is challenging without advanced international tax accounting experience.

The 4 Most Common Mechanisms for Double Tax Relief

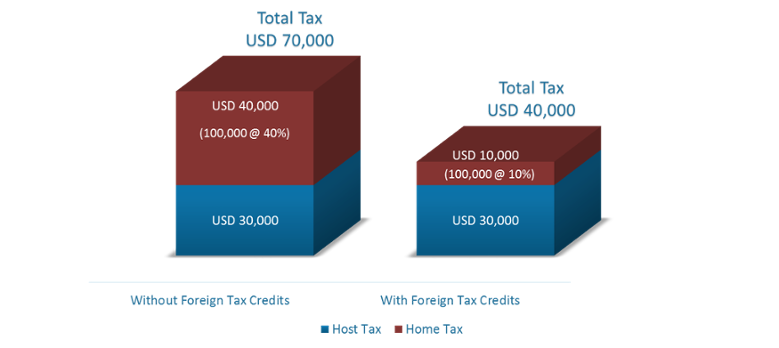

a) Foreign Tax Credit (FTC)

The home country offers a credit for taxes paid to a foreign country. FTC is generally claimed in the home country where tax residency continues, for certain host taxes paid. Typically, this credit is limited to the amount of the home tax on the income being taxed twice. For example, the host tax is assessed at 40% on the income earned during assignment, but the home tax rate is 30%. The FTC would be limited to 30% on the assignment income (the graphic below illustrates this effect on double-taxed income of USD 100,000).

b) Exemption with Progression

Common in Europe, this approach to double tax relief considers the progressive tax rate when calculating the home tax for remaining non-assignment income. Typically, this results in a different home tax than using the foreign tax credit method. (The graphic below illustrates this effect on total income of USD 100,000, double-taxed income of USD 30,000, and a home tax rate with two tax brackets).

c) Exempt from Host Country Tax applying Host Tax Law

An employee may be exempt from host tax based upon taxability thresholds such as a minimum taxable income, a minimum number of days present in the host country, or both. These exemption thresholds typically are to be used in shorter-term business traveler arrangements. In addition, it may be possible to qualify for host tax exemption based on an employee’s visa, work activities, or other status. For example, certain humanitarian workers and foreign diplomatic government workers are granted exemptions from taxes.

d) Exempt from Host Country Tax applying Tax Treaty Rules

Tax treaties are agreements between countries to coordinate the tax laws involving cross-border taxation. The general rule is that employment income is taxed where the services are performed – the host country in the case of international assignments. However, if all criteria is met, the income is exempt from host taxation and subject to tax only in the country of residence – the home country. Generally there are 3 basic criteria to meet the tax treaty exemption:

- Present in the host country for 183 days or less – within a tax year, or more commonly, within any 12-month period, and

- the employee is not on the host country payroll, and

- the costs of the employee’s compensation cannot be charged back to the host country employer.

The application of the tax treaty rules are complex, and requires a sound understanding of the company’s tax situation as well as the employee’s time spent in the host country.

Seite drucken

Seite drucken